Predictive analytics is reshaping how small and medium enterprises (SMEs) access credit. Traditional methods often rely on outdated financial data, leading to slow approvals and missed opportunities for businesses. By using real-time data like bank transactions, tax filings, and digital activity, predictive models offer faster, more accurate credit assessments.

Key takeaways:

- Improved Speed: Loan decisions now take hours instead of weeks.

- Better Accuracy: Predictive models increase approval rates by 10%-35% while reducing portfolio losses by 15%-40%.

- Increased Access: SMEs with limited credit histories are now evaluated using operational data, broadening their funding opportunities.

Success stories include First Hawaiian Bank boosting instant approvals from 4% to 40% with AI, and Bradesco cutting loan approval times from 10 days to 3.3 days. These examples highlight how data-driven tools are transforming SME lending, ensuring faster decisions and reduced risks for lenders.

Forward-Implied SME Credit Risk Signals - Recognition and Use

sbb-itb-bec6a7e

SME Credit Risk Challenges and the Case for Predictive Analytics

Predictive Analytics vs Traditional Credit Evaluation for SMEs

Key Challenges in SME Lending

Small and medium enterprises (SMEs) face a unique set of challenges when it comes to securing credit. Unlike large corporations, they often lack audited financial statements, substantial collateral, and long credit histories. This makes it tough for traditional lenders to evaluate their creditworthiness effectively.

Globally, this has created a $4.9 trillion financing gap [4]. In India alone, 86% of the country's 63 million MSMEs are unable to access formal credit, contributing to a staggering $530 billion gap projected by 2026 [2]. As CarmaOne aptly highlighted:

"The $530 billion credit gap is not a failure of demand. It is a failure of assessment infrastructure." [2]

Traditional lending methods exacerbate the issue. The underwriting process typically demands 15–20 documents and can stretch over 3–4 weeks [2]. For a small business owner needing a working capital loan to fulfill an order, such delays could mean the difference between seizing a growth opportunity and losing it altogether. Beyond credit, leveraging essential AI tools for small business growth can help bridge other operational gaps.

These hurdles reveal the weaknesses in conventional evaluation methods and underscore the need for a more effective approach, often starting with how to implement AI in your SME.

Why Standard Credit Checks Fall Short

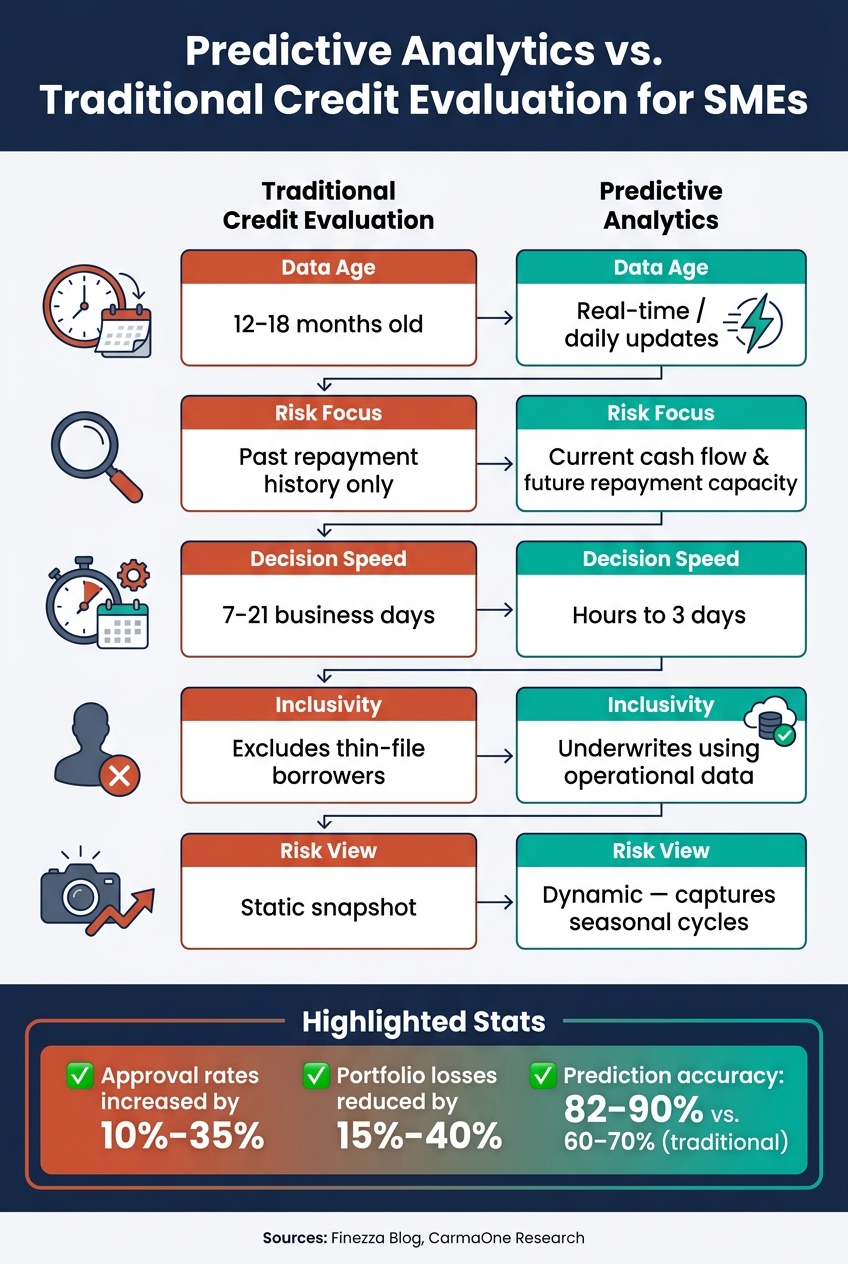

Conventional credit scoring relies on outdated financial data, which often fails to reflect an SME's current performance. For instance, audited financial records reviewed by lenders are usually 12 to 18 months old by the time they are assessed [7].

"Lenders who rely primarily on audited financials are assessing the borrower as it was, not as it is. The gap between those two states is precisely where MSME defaults tend to originate." - Finezza Blog [7]

This approach is particularly problematic for seasonal businesses, where a slow quarter is often misinterpreted as a sign of risk. In the UK, for example, banks reject 80% of loan applicants with thin credit profiles, many of whom are actually low-risk borrowers. This results in an estimated $4 billion in missed lending opportunities [8].

Predictive analytics offers a way to bridge these gaps. Unlike traditional methods, it uses real-time data - such as bank transactions, GST filings, and digital payment patterns - to evaluate a business’s current standing and future potential. By leveraging this approach, lenders have increased approval rates by 10% to 35% without taking on additional risk. At the same time, portfolio losses have decreased by 15% to 40% [8].

| Dimension | Traditional Credit Evaluation | Predictive Analytics |

|---|---|---|

| Data Age | 12–18 months old | Real-time / daily |

| Risk Focus | Past repayment history | Current cash flow & future capacity |

| Decision Speed | 7–21 business days | Hours to 3 days |

| Inclusivity | Excludes thin-file borrowers | Underwrites based on operational data |

| Risk View | Static snapshot | Dynamic, captures seasonal cycles |

Success Stories: Predictive Analytics in Practice

Real-world examples highlight how predictive analytics is transforming credit risk management. These case studies showcase how businesses have tackled SME credit challenges using advanced tools and data-driven strategies.

Case Study 1: Cash Flow Forecasting for SME Lending

Hunt Electric Corporation, an electrical contractor based in Minnesota, struggled with unpredictable cash flows from large projects. These fluctuations disrupted borrowing plans and made it difficult to take advantage of early-payment discounts from suppliers. To address this, the company adopted a machine learning model to forecast invoice payment dates and future labor costs. The model considered variables like unionized labor rates, seasonal trends, and multi-state tax obligations [9].

The results were immediate and impactful. CFO Ron Somerville shared:

"We've reinvented our cash planning process with Machine Learning. It has dramatically improved the accuracy of our outlook, which removes risk, and allows us to take on new projects with confidence." [9]

This shift led to reduced Line of Credit borrowing costs and better capture of early-payment discounts. For SME lenders, this example emphasizes the power of leveraging transactional and operational data to assess repayment capacity effectively.

Case Study 2: Early Default Detection for Portfolio Stability

Bradesco, one of Brazil's largest banks, implemented an AI-driven credit strategy using machine learning tools from Kunumi, a startup it had acquired. The goal was to identify at-risk accounts early and enable swift intervention. By April 2026, the bank had cut wholesale loan approval times from 10 days to just 3.3 days and automated 20% of renegotiation proposals for mid-sized companies [3].

This approach not only sped up decision-making but also stabilized the portfolio. Early detection of potential defaults allowed the credit team to act before risks escalated. Rafael Cavalcanti, Bradesco's Director of Data Intelligence, highlighted the financial gains:

"With the first batch of Kunumi's solutions now maturing, we are already seeing results of R$250 million." [3]

The bank's default rates declined and stabilized, proving that faster decisions can still maintain or even improve portfolio health.

Case Study 3: Automated Credit Scoring for Faster Approvals

First Hawaiian Bank partnered with Zest AI to upgrade its credit scoring process between 2025 and 2026. Previously, 90% of applications required manual review due to the limitations of a national scoring model. Within just four months, the bank deployed a custom machine learning model built on millions of data points [6].

The results were striking:

| Metric | Before | After |

|---|---|---|

| Automated decisioning rate | 4% | 55% |

| Instant approval rate | 4% | 40% |

| Overall approval rate | Baseline | +15% |

| Delinquency performance | Baseline | 4x better performance |

Automated decisioning rates jumped from 4% to 55%, and accounts approved using AI scores outperformed manually reviewed accounts by four times in delinquency performance [6]. This case underscores how automation can drive efficiency while reducing risk.

Case Study 4: Risk Segmentation for Smarter Credit Limits

Edward Don & Company, a U.S. foodservice distributor with $600 million in revenue, adopted AvantGard Predictive Metrics between 2024 and 2025. By moving away from generic bureau scores and instead using statistical models based on internal accounts receivable data, the company gained a clearer perspective on customer credit risk [10].

Before implementing the new model, 66.2% of accounts were labeled as high risk and placed on hold. Post-implementation, that number dropped to just 14.1%, allowing the credit team to focus on genuinely risky accounts. John Fahey, the company’s Director of Credit, explained:

"Statistical-scoring helped us identify that on average only 14.1% of our accounts were truly high risk, and needed to be on hold. This freed up our credit analysts' time to focus on those accounts as well as other projects." [10]

The project also led to a 5.3-day reduction in Days Sales Outstanding (DSO) and a 25% boost in collection call productivity [10]. These results demonstrate how predictive analytics can streamline operations and improve outcomes across the board.

Methods and Results Across Case Studies

Predictive Methods Used

The case studies explored here rely on three main approaches: machine learning, statistical scorecards, and automated decision engines. Each of these methods taps into high-quality, real-time data, which has been a game-changer for achieving better outcomes.

Traditional scoring methods were cumbersome, requiring piles of documentation and long processing times. In contrast, AI-driven models can use alternative data - like GST filings or bank transactions - to auto-approve loans in just 2–4 hours. These models boast an accuracy rate of 82–90%, compared to the 60–70% accuracy of older methods [2].

Real-time monitoring is another key feature, keeping an eye on signals like filing delays or revenue drops. This allows lenders to detect financial stress 2–6 months before a potential default [2].

Transparency is essential in these processes. While logistic regression is still popular for its ease of interpretation, more advanced techniques like gradient boosting models (e.g., LightGBM) offer superior accuracy. For example, using external public data - such as government credit records or court verdicts - these advanced models achieved an AUC of 0.92 [11].

The impact of these methods is clear in the measurable outcomes, summarized in the table below.

Case Study Outcomes Compared

The table below showcases how these predictive methods led to real-world improvements for different organizations:

| Organization | Challenge | Key Data Inputs | Predictive Method | Outcome |

|---|---|---|---|---|

| Bradesco | Slow wholesale credit approvals; default risk | Internal datasets | ML with synthetic data | Approval times cut from 10 days to 3.3 days; R$250M in matured results [3] |

| CGC Malaysia | Slow manual processing; lack of collateral | Bureau and demographic data | FICO Blaze Advisor (decision rules) | NPL rate maintained at 3% [5] |

These examples underline the importance of high-quality, relevant data over the complexity of the model itself. For instance, Bradesco used synthetic data to address gaps in historical credit data, leading to faster approvals and significant financial gains [3]. Meanwhile, CGC Malaysia employed decision rule engines to keep its portfolio stable despite challenges [5].

"What used to take six months now takes three. We have even tested models built overnight and compared them with official models developed by data scientists, and the results are very similar." - André Duarte Oliveira, Head of Credit, Bradesco [3]

Across the board, replacing static risk labels with dynamic, data-driven segmentation has transformed the way lenders assess borrowers. This shift has not only sped up approvals but also improved overall portfolio stability.

Conclusion: What Predictive Analytics Means for SME Credit Risk Management

The evidence is clear: predictive analytics is transforming SME lending. Take, for example, an African e-commerce platform that scaled its loans from 1,000 to 40,000 in just six months [1]. Or Propel Credit, which managed to cut its non-performing assets by 67% while keeping loan decisions under 30 minutes [12]. These examples share a common thread - leveraging better data leads to better outcomes for both lenders and borrowers.

Three standout benefits are driving this shift:

- Speed: Loan decisions that once took weeks now happen in hours.

- Accuracy: Prediction rates have jumped from 60–70% to an impressive 82–90% [2].

- Inclusion: Thin-file SMEs are gaining access to credit, with 90% of Fundfina customers reporting increased earnings after receiving analytics-driven loans [4].

For SMEs, the takeaway is simple: keep your financial records accurate and digitized. Lenders increasingly depend on real-time data, such as bank statements, tax filings, and transactional histories, to assess creditworthiness. The more organized and accessible your data, the faster and more favorable your evaluation will be.

For lenders, the focus is shifting toward ongoing monitoring after loans are disbursed. This continuous oversight, rather than relying solely on initial credit checks, is proving to be a game-changer in reducing non-performing assets.

To get started, both SMEs and lenders can explore platforms like AI for Businesses, which offers a curated directory of AI tools tailored to improve operational efficiency. Finding the right tool to tackle your specific credit risk challenges is a practical step toward achieving the kind of success seen in these case studies. For those ready to implement these solutions, learning how to run an AI pilot can help minimize risk while maximizing efficiency.

FAQs

What real-time data can an SME share to improve credit decisions?

SMEs have the ability to share real-time data such as cash flow metrics, banking transactions, and invoicing patterns, which can play a big role in improving credit decisions. Platforms like Shopify, QuickBooks, or Xero offer valuable data points, including order history, balance sheets, and accounts receivable aging details.

On top of that, transaction-level data from POS systems and government-verified tax filings provide a clearer view of revenue streams, expenses, and payment behaviors. These insights can help paint a more accurate financial picture for lenders or partners.

How do lenders keep AI credit models fair and explainable?

Lenders rely on Explainable AI (XAI) tools like SHAP and LIME to make credit decisions more transparent. These methods break down complex AI-driven outcomes into understandable elements, such as a borrower's debt-to-income ratio. By doing this, they make it easier for both lenders and borrowers to grasp why certain decisions are made.

To promote fairness, lenders take extra precautions, such as eliminating proxies for sensitive characteristics (like age or race) from training data and running rigorous bias tests. Human oversight is also a key part of the process, ensuring that decisions remain balanced and ethical. For regulated lenders, creating detailed audit trails is another essential step. This helps them comply with legal standards and ensures that every AI-driven decision can be explained and justified.

What should SMEs do now to qualify for faster approvals?

To improve the chances of faster credit approvals, small and medium-sized enterprises (SMEs) should focus on a few key financial habits. Start with accurate bookkeeping - keeping detailed and organized records ensures clarity in your financial health. It's also essential to separate personal and business accounts to avoid any confusion over cash flow. A steady cash flow, free of unexplained spikes or drops, signals stability to lenders.

Reliable financial routines - such as consistently meeting recurring obligations like loan payments or bills - play a big role in how AI-driven systems evaluate creditworthiness. Regular account activity, including stable and predictable deposits, also shows lenders that your business is actively managed and financially engaged. These efforts make a strong case for faster and smoother credit approvals.